_edited.png)

Breakfast Bites - Mon Oct 2, 2023

- Oct 2, 2023

- 3 min read

Rise and shine everyone and Happy Monday!

It was certainly an eventful weekend with US Government officials rushing until late Saturday to avert a government shutdown. That’s in place now and it’s causing a relief rally in US equity futures.

Chair Powell speaks later today and it remains to be seen if there are any additional remarks that may spark a sell off.

The US Dollar Index is back up again at $106.5 with US rates rising across the board. The Yield Curve has steepened further to -0.47%. Gold is lower while Oil and Bitcoin are higher, with BTC crossing 28000 yesterday.

We have a whole host of macro data this week with PMI and ISM Activity data being released, with the week closing with the monthly US jobs report. We also have a number of Fed speakers in the queue. It’s a quiet week for earnings though with Lamb Weston and Conagra reporting on Thursday.

And… I started my week with an appearance on Bloomberg TV

Asia and Australia

Asian markets that are open are trading higher. Asian equities mostly lower Monday. Nikkei pared early gains to close slightly lower, ASX logged mild declines too. Taiwan higher underpinned by solid gains in semi stocks, southeast Asia mixed. Greater China, South Korea, India all closed for holidays.

The Bank of Japan announced another round of bond buying on Oct 4 of the 5 year and 10 year JGBs, after the 10Y yield hit the highest since 2013. The USD/JPY spiked this morning as well, closing in on 150. Japan’s Tankan survey came in positive

We received PMI data from China over the weekend. The official NBS PMIs shows that manufacturing activity has finally improved to expansionary territory rising to 50.2. The Caixin Manufacturing PMI however, came in lower than expected. (Remember, the NBS survey has a larger sample set and focuses more on the larger firms, while the Caixin survey focuses on private firms and exporters).

World Bank lowers China’s growth forecasts, focusing on the slower growth and perils of the property market. The forecast for 2023 remains at 5% but, for 2024, the forecast has been reduced to 4.4% from 4.8%. They said: “Asia faces one of worst economic outlooks in half a century”.

RBA expected to leave cash rate unchanged at 4.10% at Tuesday's policy meeting that will be Michelle Bullock's first as governor. The announcement is at 11:30 pm ET today, Monday.

PMI data across Asia still looks weak. Philippines is the only country that showed improvement and moved into expansionary territory. Indonesia remains in expansionary territory but, the level declined last month. While most these countries have paused hikes, the effect is still making its way through the system, putting pressure on economic growth and exports. Higher oil prices may make this much worse.

Europe, Middle East, Africa

European markets remain muted in this morning’s trading.

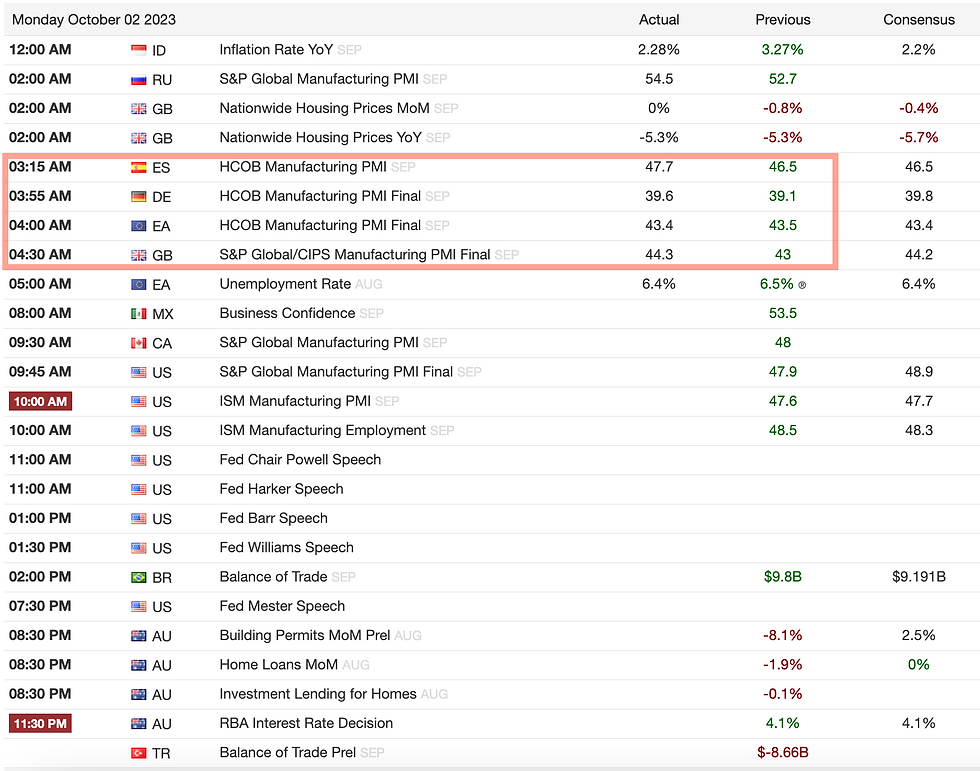

Eurozone final PMI for September remained in broad-based downturn. Final PMI was confirmed at 43.4, in-line with the preliminary release and below August's 43.5 reading.

German final PMI was 39.6 vs 39.8 preliminary and 39.1 in August. Output fell at the fastest rate since May 2020 amid further sharp drop in new orders.

UK final manufacturing PMI little changed from flash reading at 44.3 versus preliminary 44.2 outturn and prior 43.0. Signs that weakness in the manufacturing sector may have reached a trough after hitting 39-month low in August.

Minutes from the September Riksbank policy meeting signalled readiness for another rate hike in the key policy rate and said they plan to keep a restrictive monetary policy for longer in a bid to tackle inflationary pressures.

The Americas

AAII bullish sentiment fell 3.5pp to 27.8% in week-ended 27-Sep, leaving it down 14.4pp over past three weeks and lowest since 25-May. Bullish sentiment below historical average of 37.5% for sixth time in last seven weeks.

Kellogg’s breakup is set to go forward today. Kellogg (K) is spinning off WK Kellogg (KLG), the North American cereal business. Following the spin-off, the parent Kellogg will keep the global snacking business, changing its name to Kellanova and will remain in the S&P 500. WK Kellogg will replace American Vanguard in the S&P 600.

KKR has completed the sale of over 5M square-feet (SF) of industrial warehouse and distribution properties for a total aggregate value of over $560M. The dispositions were completed through five discrete transactions with five separate buyers. The fifth and final sale closed on 29-Sep

Calendar

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)

Comments